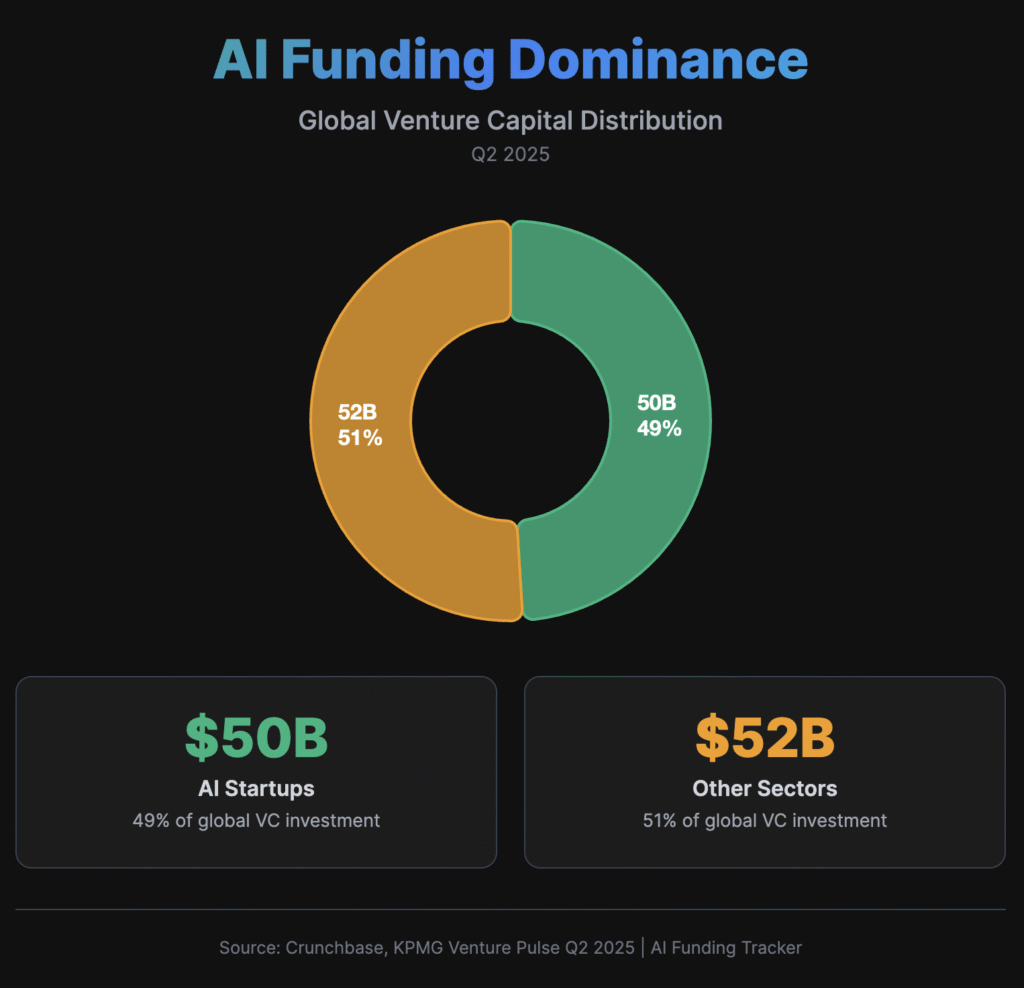

AI startups took almost half of all venture capital in Q2 2025. They raised $50 billion total, according to Crunchbase data. Scale AI led with a record $14.3 billion round from Meta. The quarter saw fewer deals but much bigger check sizes. Investors made big bets on AI infrastructure companies.

Executive Summary

- $50 billion raised by AI startups in Q2 2025 (KPMG Venture Pulse)

- 2,146 deals completed (stable from Q1)

- 16 companies raised $500M+ rounds, capturing 33% of all VC dollars

- US dominated with 85% of global AI funding

- Late-stage deals averaged $327 million (up 327% from 2023)

Top 10 Funding Rounds

| Company | Amount | Stage | Valuation | Lead Investor | Sector |

|---|---|---|---|---|---|

| Scale AI | $14.3B | Series G | $29B | Meta | Data Infrastructure |

| Databricks | $10B | Series I | $55B | T. Rowe Price | Data Platform |

| CoreWeave | $7.5B | Series C | $19B | Coatue | AI Cloud |

| xAI | $6.0B | Series B | $24B | Valor Equity | LLM Foundation |

| Infinite Reality | $3.0B | Series B | $12B | Liberty Media | Metaverse AI |

| Character.AI | $2.7B | Series D | $5B | A16Z | Consumer AI |

| Anduril Industries | $2.5B | Series G | $14B | Founders Fund | Defense AI |

| Safe Superintelligence | $2.0B | Series A | $10B | A16Z | AI Safety |

| Thinking Machines | $2.0B | Seed | $8B | Sequoia | General AI |

| Anysphere | $900M | Series C | $4B | Thrive Capital | AI Coding |

Funding Details

Scale AI Sets New Record

Scale AI closed the biggest VC round in 2025 at $14.3 billion. Meta bought a 49% stake in the company. This values Scale AI at $29 billion total.

What Scale AI does: They process training data for big AI models. Companies like OpenAI use Scale to clean and label their datasets. This helps train ChatGPT and other AI systems.

Why Meta invested: Meta needs massive data processing power for its AI projects. This deal gives Meta direct access to Scale’s platform. It also secures a key partnership for the future.

Databricks Reaches $55B Valuation

Databricks raised $10 billion from T. Rowe Price and other big investors. The company is now worth $55 billion. This makes it one of the world’s most valuable private companies.

What they do: Databricks helps companies analyze data and build AI models. Businesses use their platform to create AI tools with their own data.

AI Safety Gets Serious Investment

Safe Superintelligence raised $2 billion in their first funding round. The company is now worth $10 billion. They focus on building safe AI systems.

The team: Founded by Ilya Sutskever, who used to work at OpenAI. The team includes top AI researchers. They work on AI alignment and safety challenges.

Analysis & Context

Market Concentration Reaches New Levels

Q2 2025 showed extreme concentration in venture funding (EY analysis):

- 33% of all VC dollars went to just 16 companies with $500M+ rounds

- 5 companies got over one-third of all US venture funding

- Average late-stage AI deal hit $327 million vs $48 million in 2023

This shows investors prefer proven AI companies over new startups.

Corporate VCs Drive AI Investment

Big Tech companies led 75% of AI funding rounds by dollar amount:

- Meta: $14.3B (mostly Scale AI)

- Microsoft: $4.1B across 12 deals

- Google Ventures: $3.7B in 18 companies

- NVIDIA: $1.8B backing 23 startups

Corporate investors bring more than money. They offer technical help and business partnerships.

Geographic Dominance Continues

The United States kept its lead in AI funding:

- 85% of global AI funding went to US companies ($42.5B of $50B)

- San Francisco Bay Area got 70% of US investment

- Europe got less than 8% of worldwide AI funding

- China’s AI funding dropped 45% year-over-year due to new rules

Sector Evolution: Infrastructure First

AI infrastructure companies got the biggest funding share (Ropes & Gray report):

Data Infrastructure ($15.7B): Companies like Scale AI and Databricks that process and manage AI training data.

Cloud Computing ($12.3B): GPU clusters and specialized AI computing platforms like CoreWeave.

Foundation Models ($11.8B): Large language model companies including xAI and Character.AI.

Applications ($10.2B): AI-powered software for specific use cases like coding (Anysphere) and defense (Anduril).

Investment Stage Analysis

Early-Stage Funding (Seed & Series A)

- Deal count: Down 23% year-over-year

- Average deal size: $12.3 million (up 45%)

- Focus areas: Vertical AI applications, developer tools

Investors became pickier at early stages. They want teams with proven AI skills and clear market uses.

Growth-Stage Investment (Series B-D)

- Deal count: Down 15% year-over-year

- Average deal size: $67 million (up 89%)

- Focus areas: Scaling AI platforms, international expansion

Growth-stage companies with strong numbers got bigger rounds. Investors picked market leaders.

Late-Stage Rounds (Series E+)

- Deal count: Up 34% year-over-year

- Average deal size: $327 million (up 327%)

- Focus areas: AI infrastructure, foundation models, acquisitions

Late-stage AI companies got top prices. This was based on their strategic importance and market position.

Regional Breakdown

North America: $42.5B (85% of global AI funding)

Advantages:

- Deep venture capital ecosystem

- Leading AI research universities

- Regulatory clarity for AI development

- Access to technical talent

Top funding hubs:

- San Francisco Bay Area: $29.8B

- New York: $5.2B

- Boston: $3.1B

- Seattle: $2.4B

Europe: $4.2B (8% of global AI funding)

Challenges:

- Fragmented markets across countries

- Limited late-stage capital availability

- Developing AI regulatory framework

- Brain drain to US companies

Leading countries:

- Germany: $1.4B

- United Kingdom: $1.1B

- France: $0.9B

- Netherlands: $0.5B

Asia-Pacific: $3.3B (7% of global AI funding)

China led the region but saw big decline (BestBrokers analysis):

- Funding dropped 45% year-over-year

- New rules restrict AI model development

- Limited access to advanced chips

- Fewer chances for global expansion

Key Trends and Market Shifts

1. Quality Over Quantity

Investors focused on fewer, higher-quality deals:

- Total deal count decreased 12% globally

- Average deal sizes increased across all stages

- Due diligence periods extended for technical evaluation

- Revenue multiples remained elevated for top performers

2. AI Safety Becomes Investment Category

Growing worry about AI risks drove dedicated safety funding (Mintz legal analysis):

- $2.8 billion invested in AI safety and governance

- Rule compliance tools gaining traction

- Technical alignment research attracting top talent

- Government partnerships for safety standards

3. Vertical AI Applications Emerge

Specialized AI solutions gained investor attention:

- Healthcare AI: Diagnostic and drug discovery tools

- Legal AI: Contract analysis and research platforms

- Financial AI: Risk assessment and trading systems

- Defense AI: Autonomous systems and surveillance

4. Open Source vs Proprietary Models

Competition intensified between development approaches:

- Open source models like Llama challenging closed systems

- Proprietary advantages in specialized applications

- Hybrid approaches combining both strategies

- Developer ecosystem effects on adoption

Investor Landscape

Most Active VC Firms (by deal count)

| Investor | AI Deals | Total Invested | Notable Companies |

|---|---|---|---|

| Andreessen Horowitz | 47 | $3.2B | Safe Superintelligence, Character.AI |

| Sequoia Capital | 39 | $2.8B | Databricks, Thinking Machines |

| General Catalyst | 34 | $1.9B | Anysphere, Mistral AI |

| Bessemer Ventures | 31 | $1.4B | Shopify AI, Canva |

| First Round | 28 | $890M | Notion AI, Perplexity |

Corporate Strategic Investors

Big Tech AI Investment:

- Focus on infrastructure and developer tools

- Strategic partnerships beyond pure financial returns

- Talent acquisition through investment relationships

- Competitive intelligence on emerging technologies

Valuation Trends

Revenue Multiple Analysis

AI companies continued commanding premium valuations:

SaaS AI Companies:

- Median multiple: 18x revenue (vs 8x traditional SaaS)

- High-growth premium: 25-30x for >200% annual growth

- Differentiation factors: Data moats, model performance, technical team

Infrastructure Companies:

- Median multiple: 13x revenue

- Capital intensity discount: 6-8x for asset-heavy models

- Strategic value premium: 15-20x for critical infrastructure

Valuation Methodology Evolution

Investors increasingly evaluated:

- Technical differentiation: Model performance benchmarks

- Data advantages: Proprietary datasets and feedback loops

- Talent density: AI researcher and engineer concentration

- Strategic positioning: Competitive moats and partnerships

Market Outlook

Q3-Q4 2025 Expectations

Funding volume likely to moderate due to:

- Seasonal patterns: Traditional Q3 slowdown

- Investor digestion: Processing Q1-Q2 mega-rounds

- Economic uncertainty: Rising interest rates affecting valuations

- Regulatory developments: AI safety legislation pending

Sector focus shifting toward:

- Vertical applications: Industry-specific AI solutions

- AI operations: Model deployment and monitoring tools

- Edge computing: On-device AI capabilities

- International expansion: Non-US market development

2026-2027 Outlook

Market maturation expected through:

- Revenue discipline: Focus on unit economics and profitability

- Consolidation wave: Mid-tier company acquisitions

- Technical standards: Industry-wide AI safety protocols

- Regulatory compliance: Competitive advantage for prepared companies

Technology evolution toward:

- Multimodal AI: Integrated text, image, video capabilities

- Embodied intelligence: Robotics and physical world interaction

- Personalized AI: Individual model customization

- Scientific applications: Drug discovery, climate solutions

Investment Risks and Challenges

Technical Risks

- Model commoditization: Open source alternatives reducing differentiation

- Compute costs: Infrastructure expenses pressuring margins

- Talent scarcity: AI expertise driving salary inflation

- Technical debt: Rapid development creating maintenance challenges

Market Risks

- Customer concentration: Over-dependence on Big Tech partnerships

- Economic sensitivity: AI adoption vulnerable to spending cuts

- Competitive pressure: Incumbent software adding AI features

- Regulatory uncertainty: Compliance costs and restrictions

Investment-Specific Risks

- Valuation bubbles: Prices disconnected from fundamentals

- Liquidity constraints: Limited exit opportunities

- Due diligence gaps: Technical evaluation challenges

- Portfolio concentration: Over-allocation to single sector

Next Steps

For Investors

Portfolio strategy:

- Diversify across AI infrastructure, applications, and vertical solutions

- Increase technical due diligence capabilities

- Monitor regulatory developments affecting portfolio companies

- Consider international opportunities at discount valuations

Due diligence focus:

- Technical differentiation and competitive moats

- Revenue quality and customer concentration

- Team composition and technical expertise depth

- Regulatory compliance and safety considerations

For Startups

Fundraising approach:

- Raise 18-24 months of runway given longer cycles

- Emphasize unique data advantages and model performance

- Demonstrate clear path to profitability and scale

- Consider strategic investors for distribution partnerships

Competitive positioning:

- Build proprietary datasets through customer partnerships

- Focus on specific use cases rather than general solutions

- Invest early in AI safety and governance capabilities

- Plan international expansion considering regulatory differences

Conclusion

Q2 2025 marked AI’s complete dominance of venture capital markets, with the sector capturing nearly half of all investment dollars globally. The concentration of capital in mega-rounds reflects genuine technological disruption and investor conviction in AI’s transformative potential.

However, this concentration also creates risks. Extreme valuations pressure companies to deliver outsized returns while the market’s heavy dependence on AI advancement makes it vulnerable to technical setbacks or economic downturns.

Looking ahead, the AI funding landscape will likely evolve from the current “gold rush” phase toward more disciplined investment focused on sustainable business models, regulatory compliance, and measurable value creation. Companies demonstrating clear competitive advantages and paths to profitability will be best positioned for continued growth.

AI funding reached historic levels in Q2 2025, driven by breakthrough technologies and strategic corporate investment. While near-term moderation is likely, the sector’s long-term prospects remain strong for companies that can execute at scale while building defensible market positions.

FAQs

AI startups raised $50 billion in Q2 2025, representing almost half of all venture capital investment globally during the quarter.

Scale AI raised $14.3 billion from Meta in the largest venture capital round of 2025, valuing the data infrastructure company at $29 billion.

Andreessen Horowitz led with 47 deals ($3.2B), followed by Sequoia Capital (39 deals, $2.8B) and General Catalyst (34 deals, $1.9B).

US companies captured 85% of global AI funding in Q2 2025 ($42.5B of $50B total), with the San Francisco Bay Area receiving 70% of US investment.